Personal Development Goals

Personal Development Goals

Bedrooms Designed for Aging in Place

Bedrooms Designed for Aging in Place Furniture

Furniture Kitchens Designed for Aging in Place

Kitchens Designed for Aging in Place Lighting and Light Switches

Lighting and Light Switches

Assisting With Functional Mobility

Assisting With Functional Mobility Bath and Shower Mobility Aids

Bath and Shower Mobility Aids Bedroom Mobility Aids

Bedroom Mobility Aids Assisting with Personal Grooming and Hygiene

Assisting with Personal Grooming and Hygiene Caring for Someone With Incontinence

Caring for Someone With Incontinence Helping People To Cope with Alzheimer’s and Dementia

Helping People To Cope with Alzheimer’s and Dementia Helping With Bill Paying

Helping With Bill Paying Home Cleaning Services

Home Cleaning Services Offering Companionship

Offering Companionship Providing Medication Reminders

Providing Medication Reminders Providing Transportation

Providing Transportation Running Errands

Running Errands

Burn Care

Burn Care Occupational Therapy

Occupational Therapy Mental Health Rehabilitaion

Mental Health Rehabilitaion

Canes

Canes Chair Lifts / Stair Lifts

Chair Lifts / Stair Lifts Grab Bars

Grab Bars Knee Scooters / Knee Walkers

Knee Scooters / Knee Walkers Ramps

Ramps Scooters

Scooters Transfer belts / pads / equipment

Transfer belts / pads / equipment Walkers and Rollaters

Walkers and Rollaters Wheelchairs and Mobile Chairs

Wheelchairs and Mobile Chairs

Accounting and Tax

Accounting and Tax Books-Seminars-Courses

Books-Seminars-Courses

ASSISTED LIVING

ASSISTED LIVING Assisted Living Facilities

Assisted Living Facilities Cohousing Communities

Cohousing Communities Manufactured Housing Communities

Manufactured Housing Communities Naturally Occurring Retirement Communities (NORCs)

Naturally Occurring Retirement Communities (NORCs) Personal Residence LIving Independetly

Personal Residence LIving Independetly Accessory Dwelling Units

Accessory Dwelling Units Continuing Care Retirement Communities

Continuing Care Retirement Communities Multigenerational Households

Multigenerational HouseholdsFederal Employees Retirement System (FERS)

FERS is a retirement plan that provides benefits to federal government employees from three different sources:

- A Basic Benefit Plan

- Social Security

- The Thrift Savings Plan (TSP)

Social Security and the TSP can go with you to your next job if you leave the federal government before retirement. The Basic Benefit and Social Security parts of FERS require you to pay your share each pay period. Your government agency employer withholds the cost of the Basic Benefit and Social Security from your pay as payroll deductions. The agency pays its part too. Then, after you retire, you receive annuity payments each month for the rest of your life.

The TSP part of FERS is an account that your agency automatically sets up for you. Each pay period your agency deposits an amount equal to 1% of the basic pay you earn into the account. You can also make your own contributions to your TSP account, and your agency will make a matching contribution. These contributions are tax-deferred. The Thrift Savings Plan is administered by the Federal Retirement Thrift Investment Board.

Social Security

If you spent any portion of your working career in the private sector, you likely saw a significant portion of your earnings going to a tax line item called FICA, which is an acronym for Federal Insurance Contributions Act. FICA tax is the mandatory amount withheld from your paycheck to pay for Social Security retirement benefits.

While the amount you pay each year for FICA tax is tracked by the Social Security Administration, your payments are not segregated into a separate account earning interest and waiting there for you to retire. The money withheld from you is being used to pay the current benefits of retirees and others eligible to receive benefits. Payment of benefits to any group of recipients is dependent in part on receipt of the FICA tax others currently pay each month into the fund. This fact is the source of concern for many Americans approaching retirement that there will not be sufficient money paid in each year by younger workers as the tidal wave of Baby Boomers stops paying into the system and starts drawing benefits out.

While we cannot resolve the issue of whether and what level of benefits will exist in the future, we can discuss what you can expect under current rules and payout schedules.

How Social Security Works

Social Security benefits include monthly retirement, survivor and disability benefits. Retirement benefits are targeted to start when you are about 65 – 67 (“Normal Retirement Age”, or “NRA”), depending on when you were born. The monthly amount received if you begin drawing benefits at your NRA is called your Primary Insurance Amount, or PIA. Your PIA is dependent on a three-part formula that incorporates a 35-year average of the amounts that you paid into the system through FICA taxes over the course of your working career. You can elect to receive a percentage of your PIA benefits as early as 62, and any time after your Normal Retirement Age up to the age of 70, the oldest age at which you can elect to begin receiving your benefits. The earlier you elect to start receiving benefits, the lower the percentage of your PIA amount you will receive each month.

The amount of Social Security benefits that must be included on your income tax return and used to calculate your income tax liability depends on the total amount of your income and benefits for the taxable year.

The First Question – What is Your Expected Monthly Full Retirement Benefits Amount (PIA)?

Your Social Security PIA payments are calculated based on the 35 years in which you earned the most and were paying FICA tax. If you did not work 35 years, or were not working in the private sector and paying FICA taxes for 35 years, zeros are averaged into the calculation for any shortfall years, and result in a smaller payout.

If you are in your peak earning years now and have already reached the 35-year mark, you will likely boost your benefits by working more years at the higher earnings level and replacing lower earning years in the 35-year averaging calculation.

You can set up a user login and securely access information about your history of FICA tax payments and expected monthly benefits amount at the Social Security Administration website at www.ssa.gov/myaccount. Once you have your PIA number, you can start strategizing about when you want to begin drawing monthly benefits and estimating how much those benefits will be.

The Big Question – When Should You Start Drawing Benefits?

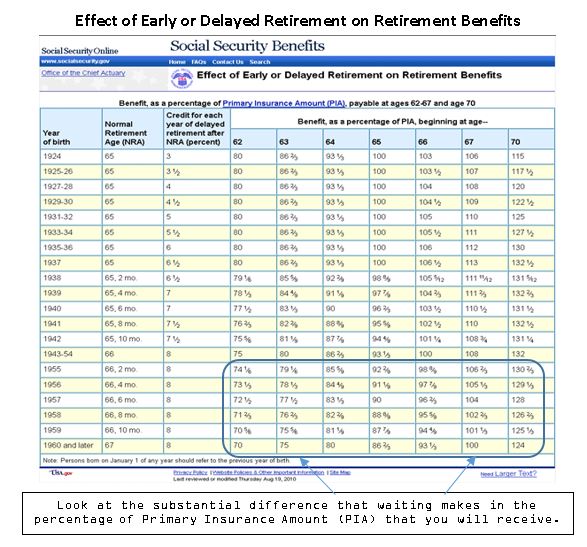

The table below was taken from the Social Security Administration website. The table shows the percentage of your expected PIA that you will receive monthly, dependent on the age at which you choose to begin drawing benefits.

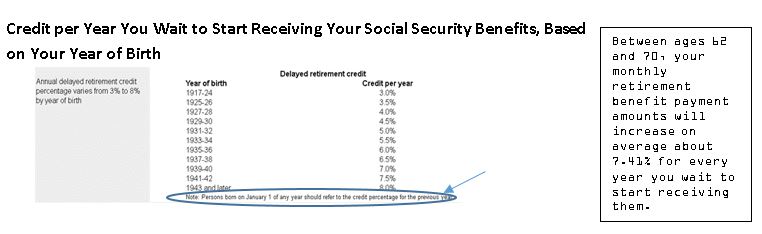

As shown in the table below, depending on the year you were born, every year you delay receiving your benefits between ages 62 and 70 increases your monthly benefits payout from 3 percent to 8 percent annually. Most importantly for the 50 – 70 year olds for whom this book is written, your monthly benefit payout will increase on average by 7.41 percent annually for every year you wait to start receiving benefits after you turn 62. Between ages 67 and 70, monthly benefits increase annually by an amount equal to 8 percent of the Normal Retirement Age PIA (Primary Insurance Amount).

If you wait until you are 70 to begin drawing benefits, your monthly benefit amounts will be about 77 percent higher than if you had started receiving benefits at age 62. On the other hand, you will have foregone receiving anything for the eight intervening years.

It is, of course, a gamble of sorts. There will be a break-even point, beyond which it will have been better for you to have waited. This age is around 80, but can be influenced by spousal issues and potential lump sum distributions.

People who claim benefits at age 62 get reduced payments over a longer number of years, while those who start benefits at 70 get much larger payments later on in retirement. When you reach the break-even age, the cumulative lifetime benefit amounts received under the two start-date scenarios will converge and become equal; if you live beyond that point, you will come out ahead by having delayed claiming benefits.

The question you need to ponder is what worries you more: the prospect that you could die early without having elected to take lower benefit payments to which you were otherwise entitled in the interim, or living beyond the breakeven point and ending up claiming far lower monthly benefits payments than you could have received later in life because you started drawing them too early? Break-even analysis influences many people to claim benefits earlier or later than they otherwise might have, because they know their family’s history and their own health and living habits. Give serious consideration to your life expectancy. Take into account family history, your eating and exercise habits, your current health, whether you smoke, drink alcohol in excess, use drugs, and other factors.

Also consider how long you plan to work, and what retirement assets you will have to draw upon. Since you effectively get a 7.41 percent boost in your monthly benefit for every year you wait to draw Social Security between 62 and your full retirement age, pulling from an IRA or other retirement account might be a wiser course than drawing Social Security early; those retirement accounts are not guaranteed to grow 7.41 percent per year.

You may not have the ability to be as strategic. If you suffer a job loss after age 62, are unable to keep up with the physical demands of your job, or your family is struggling with unemployment, high medical bills, or other unexpected expenses, you may have no choice but to apply for your Social Security benefits in order to meet your living expenses.

It will likely make sense to withdraw before the age of 70 if you have a serious health issue. If you can no longer work because of illness, or do not expect to live very long, you should probably draw at the earliest point you can.

If you have/had a physically demanding job, you may not be able to do that particular job anymore, but are not considered disabled because you can do other kinds of work. For individuals who are otherwise in good health, seeking a new job at 62 may make sense. Others might be better off drawing Social Security. You need to consider your situation, what you are capable of doing, what other resources you have, and make the right decision for you.